U.S. Industrial Manufacturing Construction Projects Worth $401B

IIR delves into the rise of electric vehicles and skyrocketing growth in the data center and semiconductor sectors.

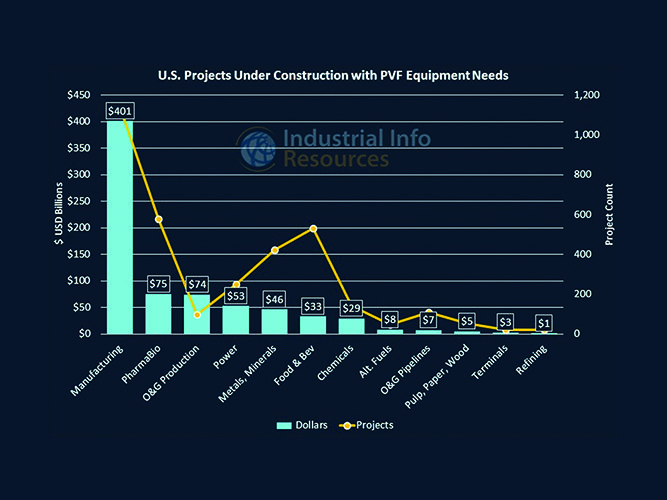

When it comes to industrial projects requiring pipe, valves and fittings (PVF), those in the industrial manufacturing sectors rule the roost regarding potential investments. Industrial manufacturing encompasses a wide range of sectors, including automotive, data centers and semiconductors, among many others.

At the time of this writing, Industrial Info Resources (IIR) was tracking nearly $740 billion worth of U.S. projects under construction with PVF requirements. Industrial manufacturing projects took the lion’s share of that amount, with $401 billion in activity.

IIR has delved into the rise of electric vehicles (EVs) and skyrocketing growth in the data center and semiconductor sectors.

EVs: Manufacturing, Sales and Batteries

The EV sector has been a significant change for the automotive industry, prompting a wave of massive spending, although this has seen some recent slowdown. Spending on this new sector has changed, particularly in the United States. Rather than a large buildout of grassroot plants for new EV models, U.S. automakers are retooling and adding equipment to existing plants to help streamline their production footprint and spend less.

However, despite the massive amount of current spending on EVs and their components, there has been a slowdown in the rate of EV sales. This is particularly true in North America, where a lack of charging infrastructure worries consumers about long-distance trips in EVs. Some EV owners are reconsidering their purchases after experiencing some of the downsides of EV ownership.

The lack of charging infrastructure in the United States is not being helped by a massive buildout of power-hungry data centers as people increasingly turn online for a variety of activities, including artificial intelligence (AI) applications. Power companies feel the pinch between providing power for new data centers or charging stations, and data centers seem largely to be winning, at least in the country’s interior.

Another element inhibiting consumers from EV purchases is the higher cost of electric vehicles, largely due to the price of the batteries. Lithium-ion battery demand is growing rapidly, and costs could come down as production rises. Lithium-ion battery demand is forecast to move from 700 gigawatt-hours in 2022 to 4.7 terawatt-hours (TWh) in 2030 and up to 20 TWh by 2050.

How the battery sector responds to this remains to be seen as demand is projected to grow sharply, but the growth rate for EV sales has slowed, potentially leading to an oversupply of EV batteries should too much battery production capacity be built.

Overall, the automotive sector remains strong, but there is some uncertainty about its direction as the EV market matures. At the same time, EV-related projects account for more spending than internal combustion engines (ICEs), traditional vehicles still make up the bulk of sales in most of the world.

Over the last year, as EV sales failed to meet the targets initially projected, automakers have been scaling back their EV ambitions. Several companies have downshifted the scale and pace of their transition to electric transportation.

It’s too early to determine whether any of that will change substantially with the Biden administration’s grants of $1.7 billion for automakers in eight states to manufacture EVs, batteries and other clean transportation equipment.

U.S. sales of electrified vehicles, including cars, trucks and motorcycles, shot up 40 percent in 2023 to about 1.4 million units from 1 million in 2022. However, that growth was not as high as some had predicted, and 2024 sales to date suggest many consumers remain skeptical about EVs.

Second-quarter 2024 U.S. EV sales grew 11.3 percent year-over-year, reaching a record-high volume of 330,463 units, according to new estimates from Kelley Blue Book. Even so, first-half sales of EVs were only about 600,000 units. On an annualized basis, 2024 sales may come closer to 2002’s 1 million than 2023’s 1.4 million.

Earlier this year, global management consultant McKinsey & Co. surveyed potential and actual EV owners for their views on electric transport. The survey included 36,964 EV owners around the world. The firm found nearly half — 46 percent — of U.S. EV owners said they were likely to switch back to vehicles powered by an ICE when they bought their next vehicle.

The top reasons EV owners around the world said their next vehicle purchase was likely to be an ICE vehicle included:

Public charging infrastructure not yet good enough for me (35 percent of worldwide survey respondents);

Total costs of ownership too high (34 percent);

Driving patterns on long-distance trips too much impacted (32 percent);

Cannot charge at home (24 percent);

Needing to worry about charging is too stressful (21 percent).

The U.S. Infrastructure Improvement and Jobs Act of 2021 included about $7.5 billion in funding to build an EV charging network. Its goal is to have 500,000 chargers in the United States by 2030. However, getting that money into the field is neither quick nor easy.

Power Use: Data Center and Semiconductor Sectors

The outlook for the data center and semiconductor sectors is not only contingent on one another in many ways but has shown similar growth trends over the past few years, with spending in both sectors escalating rapidly during and in the aftermath of the onset of the COVID-19 pandemic.

During the height of COVID, people shifted rapidly online for everything from shopping to learning to working to socializing. Suddenly, the data centers and chips that drive these interactions became of paramount importance, and a wave of construction began.

In addition, as the pandemic unfolded, consumer spending shifted to encompass a large amount of consumer electronics used in the phones and computers that kept us connected. Shipping semiconductors from their manufacturing sites (primarily in Asia) to the rest of the world became difficult as worker health and social distancing requirements impacted the means of manufacturing and shipping.

Reshoring semiconductor manufacturing sites to domestic locations became paramount to getting the chips to the manufacturers that needed them.

In addition, new challenges and headwinds are emerging for both sectors as technologies such as AI become more mainstream.

As technology has evolved, so have data center types. Many data centers are home to co-location services that provide space for the data needs of multiple companies. While all data centers use large amounts of power, this type is the least power-hungry.

Moving up the chain are facilities specifically geared toward mining Bitcoin and other cryptocurrencies. While these data centers typically have a smaller physical footprint and often use modular construction methods, they generally use more power than the typical co-location facility. The most power-hungry of all data centers are those used for AI applications; these can use up to five times the power of other data centers.

Power use in data centers is of prime importance and guides trends in the sector. For example, as many data center companies want to make their environmental footprint greener, they arrange purchase agreements and work with power developers to provide renewable energy for their facilities.

Demand is also placed on the oil and gas sector to provide the fuel needed for these operations. Power supply can be a constraining factor where supply may not be enough to meet anticipated demand.

While data centers are typically short-lived projects, often moving from planning to completion within 18 months, power generation and transmission projects take much longer to permit than a data center does, putting a constraint on the power supply for new data centers.

Many developers are considering on-site renewable energy generation, and cutting-edge power sources such as geothermal power (depending on location) and small modular reactors are being considered as future means of power.

Power demand required by U.S. data centers is expected to rise from 17 gigawatts (GW) to 35 GW by 2030. Whether the power industry can keep up with this growth is important for future development.

Like data centers, semiconductor plants have seen strong investment since the onset of COVID-19. This is expected to continue growing in the coming years as the tech sector develops and new technologies emerge.

Many of the world’s semiconductors are produced in China and Taiwan, near automotive and electronics manufacturing sites, but the sector’s footprint is becoming more widespread. A prominent example of this is the rapid development of semiconductor fabrication plants (fabs) in the United States when the CHIPS and Science Act of 2022 began providing tax incentives for the construction of new fabs.

Two of the sector’s biggest players, Intel and Taiwan Semiconductor Mfg. Co., have combined active projects worth more than $120 billion in the United States alone and $214 billion worldwide.

The data center and semiconductor sectors strive to develop the latest technologies while balancing energy consumption and environmental, social and governance ambitions. The two sectors are seeing rapid development in all parts of the world.

Brian Ford is editor in chief at Industrial Info Resources and has been with IIR since 2014. With global headquarters in Sugar Land, Texas, and 18 offices worldwide, IIR is a provider of global market intelligence specializing in the industrial process, heavy manufacturing and energy markets. To contact IIR, visit www.industrialinfo.com or call 713-783-5147.

Featured Video

PVI’s Dynamic Water Heating

Industry Events

-

07Dec

2024 HARDI Annual Conference

Atlanta, GA -

10Feb

2025 AHR Expo

Orlando , FL -

18Feb

WWETT 25

Indianapolis, IN