Distribution Trends E-Commerce Adoption

Drivers include increasing revenue, improving customer experiences, boosting efficiency and productivity — and coping with COVID-19.

The adoption rate of e-commerce in wholesale distribution soared in 2020 with a weighted 26.3 percent increase from 2019 to 2020, notes Distribution Strategy Group’s ninth annual “State of eCommerce in Distribution” survey from October-December 2020. The research provides a benchmark for the adoption and drivers of e-commerce in the wholesale distribution industry.

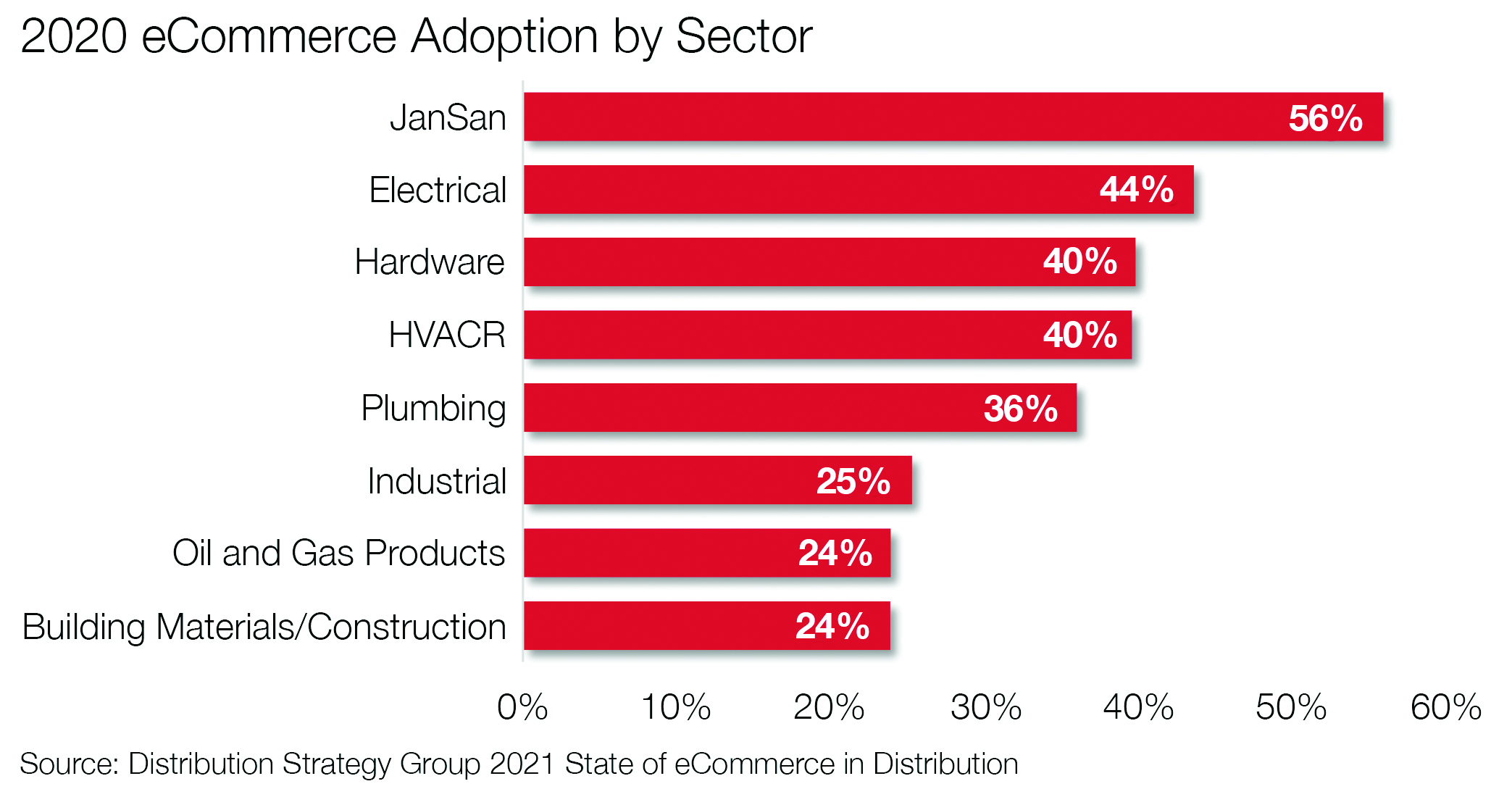

The percentage of distribution companies offering e-commerce varied widely, depending on both company size and sector. About 36 percent of plumbing distributors had e-commerce in place in 2020, while about 40 percent of HVACR distributors did. The janitorial-sanitation (jan-san) sector leads with more than half of companies offering e-commerce.

About one-quarter of companies under $50 million offer e-commerce; nearly half (47 percent) of companies larger than $1 billion do. The increase in e-commerce in the under $50 million category is staggering: from 13.4 percent in 2019 to 25.1 percent in 2020 — an 87.3 percent increase. Smaller companies have resisted e-commerce for a variety of reasons, from cost and lack of appropriate personnel to lack of product data.

But in 2020, buying groups and associations tackled the difficulty of securing product data and, in many cases, working to provide quality and affordable e-commerce platform options. Throw in the COVID-19 pandemic and many smaller distributors understood that to continue serving customers well, they have to add e-commerce as a channel.

Drivers of E-Commerce Adoption

Priorities for e-commerce implementations fell into two categories: financial and operational.

Respondents’ top two financial priorities for e-commerce include:

Growing revenue with existing customers;

Growing revenue with new customers in existing geographies and customer segments.

These make a lot of sense given that generally, most business growth comes from the areas in which you already have the most success. Many other research reports documented that adding an e-commerce channel helps the entire channel mix grow. One study by Google suggests omnichannel customers have a 30 percent higher lifetime value than those who shop using only one channel.

Distributors’ top two operational priorities for e-commerce include:

Improve ease of use and customer experience;

Increase efficiencies and productivity.

Distributors’ clear priority operationally is to improve the customer experience. Combining both the highest and second priority, 68 percent of respondents noted improving customer experience as a top priority.

Less than a third cited the customer experience as a top priority in the 2019 survey. Given the accelerated digital focus due to the pandemic, the shift this year is not surprising. Also, user experience on a website has become more critical as a primary channel for many buyers — both shopping and buying.

The Pandemic’s Impact on B2B Buying

In our survey this year, we asked respondents to tell us what percent of sales were purchased electronically by customers. Electronically was defined as via website, electronic data interchange, punchout or email. We found that post-COVID electronic purchasing is not expected to retract to pre-COVID or even during-COVID rates.

The data from this survey’s respondents is shocking: On average, distributors and manufacturers expect orders placed electronically post-COVID to increase 31 percent over pre-COVID days. Clearly, these respondents believe that not only is increased online purchasing here to stay, they expect it to grow even over what is occurring during the pandemic.

The industrial segment leads the pack among these respondents, with the HVACR sector the lowest. But each sector shows a big increase from pre-COVID to during the pandemic, then again to post-pandemic.

It is a clear indication that the increased online ordering is not just a temporary phenomenon but a long-lasting trend. COVID-19 accelerated the percentage of online ordering by three to five years.

Gaining E-Commerce Traction

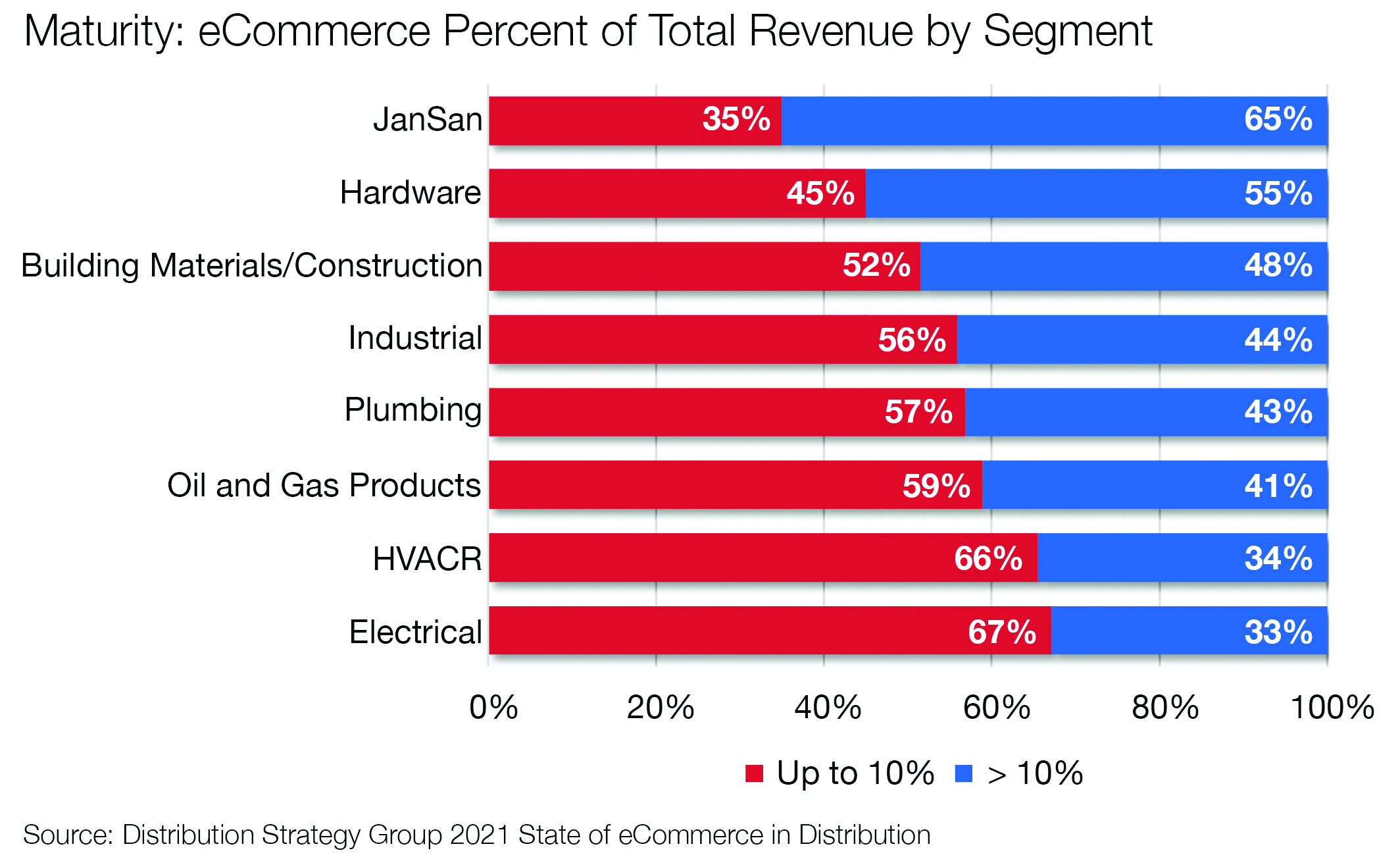

E-commerce maturity, a measure of the percentage of sales going through e-commerce for a distributor, increased significantly in 2020. With that, a new milestone has been reached for the first time: Half of respondents said e-commerce revenues were greater than 10 percent of total sales, or mature.

Companies getting into e-commerce without the continued investment and effort are generally those that will not gain traction and remain in the nascent stage (under 5 percent of total sales).

By sector, jan-san leads again. A high percentage of SKUs in this segment can be merchandised fairly easily online, driving adoption and maturity levels in this space. Among plumbing distributors (with e-commerce) surveyed, 57 percent said they had up to 10 percent of sales going through e-commerce in 2020; 43 percent had more than 10 percent, indicating maturity.

Two-thirds of HVACR distributors had up to 10 percent of sales through e-commerce in 2020; 34 percent said they had more than 10 percent.

Gaining traction in e-commerce requires continued resourcing and effort. It was clear in distributors’ responses to our survey that many still struggle to do that:

“Fundamentally, we lack an e-commerce strategy.”

“We need a better onboarding process.”

“E-commerce takes a real commitment. It is much harder than expected.”

In short, distributors conclude that while they have built the technology, customers won’t automatically come.

Strategies for E-Commerce Success

About three-quarters of the companies in the survey could be more satisfied with their e-commerce. These companies generally fall into three categories of deficiencies:

1. Not using the right technology;

2. Do not have adequate product or pricing information;

3. Inadequate marketing.

There are other deficiency categories; however, these are the big three. Distributors should act to gain traction with e-commerce based on where they are in their e-commerce journeys.

Nascent stage (less than 5 percent of sales through e-commerce): This stage is about laying a foundation for growth through e-commerce.

1. Complete an analytical customer profile, understanding your profitable sweet spots.

2. Understand how customers want to shop (research, find and select) and buy products.

3. Have a clear value proposition.

4. Develop a demand generation strategy, including inbound and outbound components.

5. Create a search engine optimization (SEO) strategy and plan, starting with an SEO audit.

6. Test and measure activities to continually adjust and optimize.

Growth stage (5 percent to 10 percent of sales through e-commerce): This stage is about building up from that foundation, gaining momentum with the channel.

1. Ensure your foundation is solid; adjust as needed.

2. Develop and implement a search engine marketing (SEM) plan (paid search).

3. Begin modifying key product content to increase the chance you will be found in search engines. Your value proposition will help you identify which content you should focus on for your customers.

4. Consider landing pages or other content appealing to key customer segments.

5. Optimize local SEO, which is often overlooked but a good opportunity to increase awareness and business at the local branch level.

6. Implement user experience improvements.

7. Evaluate and implement a proactive inside sales team. A solid e-commerce initiative supports activities in other channels.

Maturity stage (10 percent to 20 percent of sales through e-commerce): This level means that as you build, you’ll accelerate economies of scale with e-commerce and increase the distance between you and your competitors faster.

1. Ensure your foundation is solid; adapt as needed.

2. Continually test, measure and adjust activities.

3. Improve user experience, a never-ending and critical task.

4. Optimize SEO, another task that will never end.

5. Evaluate punchout integration with enterprise resource planning tools. If you haven’t already considered this, understand which customers may need punchout capabilities; these are usually the largest customers. Punchout opens up the opportunity to become sticky with customers, making the barrier to leave you high.

6. Aggressively implement SEM activities to solidify existing customers and open up new markets.

Leader stage (greater than 20 percent of sales through e-commerce): Very few distributors are in this stage of e-commerce maturity.

No matter the stage, distributors should never stop testing, measuring and adjusting, as well as improving user experiences and SEO. At the leader stage, they also should implement personalization strategies, if they haven’t already.

While e-commerce adoption rose sharply in 2020, there is plenty of runway left. Nearly three-quarters of smaller companies ($10 million to $50 million) still do not have e-commerce. And about half of the largest companies don’t have it.

But the time to adopt and make a difference in the market is now shorter. We’ve made about five years’ worth of progress in less than 12 months. You need a digital platform that enables more efficient and effective shopping and buying for your customers. And if you already have one or are building one, you need to invest in broader capabilities, marketing tools and organizational alignment to drive maturity for your organization.

Access the full report and data at www.distributionstrategy.com.

Featured Video

PVI’s Dynamic Water Heating

Industry Events

-

07Dec

2024 HARDI Annual Conference

Atlanta, GA -

10Feb

2025 AHR Expo

Orlando , FL -

18Feb

WWETT 25

Indianapolis, IN